Economy, Real Estate on Pause

The Micro View

Take me back! Just two short months ago, I was sitting in my room in the Marriott Marquis, high above bustling Times Square. I was attending what’s arguably the largest real estate conference in the world, where roughly 4,000 attendees converged from all over the globe.

There was representation from the Netherlands, France, Canada, Italy, and yes…even China, along with so many other faraway places. We eagerly crowded around communal coffee stations every morning and then jam-packed ourselves into tightly crowded rooms to better learn our industry and hone our craft, day after day. The energy was palpable as we shared our knowledge, experience, and goals. We networked, socialized, imbibed, and even danced without a care in the world, as we took our new-learned knowledge back to our cities to be the best at our craft.

Las Vegas is on hold and we’re running out of money.

Fast forward to today and New York City is in a complete shutdown, along with 50% of the world, as a result of the COVID-19 pandemic. The events over the last 60 days play over and over in my mind in both warp speed and slow motion simultaneously, like a Wes Craven film with imaginary coronavirus spikes in every scene. Overdramatic? Maybe. Maybe not.

Las Vegas is on hold and we’re running out of money. With the news of 30 more days of the state’s lockdown, many Las Vegans went into panic mode after they were struck with the sobering reality of missed paychecks. According to news reports, most casino employees ran out of pay on Friday and would be tapping into sick pay, if eligible, until that runs dry as well. There are emergency unemployment benefits in place for gig workers, yet as of this publication date, a visit to the state’s unemployment site online is greeted with a COVID-19 screen that states that all three types of emergency unemployment benefits are “Awaiting Federal Guidance.”

When the Nevada Unemployment Insurance site is up and running, it displays a notice that the State is awaiting further details from the Federal government.

That site was last updated March 31, 2020. While we optimistically reported last week the passing of a series of federal relief packages, the rollout has been wrought with defects and breakdown in implementation. The CARES (Coronavirus Aid, Relief and Economic Security) Act provides states with funding for items such as administrative costs to process the unprecedented number of unemployment claims. In spite of this, the lines are continually busy, sites keep crashing, and frustrations are running high. Patience is the mantra of the hour.

Mom and Pop businesses are the local lifeblood of Las Vegas, but under current circumstances, they’ve been picked up by the ambulance and transported to the hospital, where they have been sitting idly for days waiting to be admitted.

There is very little to report on the SBA emergency relief loans, except that they are still “under construction.” Most banks are unwilling to take applications at this time, as they are awaiting further guidance from the SBA and the U.S. Treasury, in spite of an announced April 3 rollout by the White House. Mom and Pop businesses are the local lifeblood of Las Vegas, but under current circumstances, they’ve been picked up by an ambulance and transported to the hospital, where they have been sitting idly for days waiting to be admitted. How much longer will they be able to hang on before all hope, and finances, are gone?

The mortgage protection piece of the legislation has been met with ambiguity, to say the least. Firstly, these protections only apply to federally-backed mortgages. While they represent the majority of mortgages, most homeowners are unaware of this point. Loan servicers have been announcing, en masse, 60 or 90-day payment forbearance (temporary postponement of mortgage payments), yet recent legislation provides much larger scale protection. Under the CARES Act, the borrower need only call the loan servicer and affirm hardship due to COVID-19 without the need for further documentation.

The forbearance is not discretionary. The initial time period is 180 days, with allowance for an additional 180-day extension, for a total of 12 months. The limited protection further stipulates a foreclosure moratorium, which expires on May 18, 2020. To quote the Consumer Financial Protection Bureau, “First, your lender or loan servicer may not foreclose on you for 60 days after March 18, 2020. Specifically, the CARES Act prohibits lenders and servicers from beginning a judicial or non-judicial foreclosure against you, or from finalizing a foreclosure judgment or sale, during this period of time.”

It’s critical to point out, again, that forbearance does not equate to forgiveness. Unless a borrower can successfully negotiate a loan modification of their terms (hopefully they’re doing this while they are in forbearance), these payments will keep racking up and be due and payable in one lump sum upon expiration. For example, a $1,400/mo mortgage payment in deferment for twelve months equates to a $16,800 lump sum payment. This equation, alone, does not resolve the local liquidity crisis, but it is a much-needed time out.

Can we keep homeowners in their homes long enough while we repair and rebuild the economy?

Taking what we “know” about unemployment, the possibilities of gainful employment sometime in the second quarter, the CARES Act stimulus, a national housing shortage, a healthy pre-coronavirus Las Vegas housing market, pent-up market transactions, low-interest rates, and consumer confidence, what will be the fate of our housing market in Southern Nevada is anyone’s best guess right now. Can we keep homeowners in their homes long enough while we repair and rebuild the economy? It’s a solid “I think so!” Timing, consumer education, and advocacy are critical right now, as we only have a couple of months to build viable plans of action with working portals and distribution for those individuals impacted.

Prior to the pandemic, Las Vegas was reporting a 1% default rate on mortgages, which is a very good foundation for healthy homeownership. Also notable is their moving habit trends, which started to shift about a decade ago. Las Vegans are staying in their homes for longer periods of time – approximately two years, stretching the average time in one home to roughly six to seven years. That, coupled with stricter lending practices, means most homeowners today are sitting on an enticing amount of equity that will likely outweigh the benefits of deferred mortgage payments and strategic defaults. This, inevitably, can push a higher inventory of homes on the market in a couple of months, thus creating a buyer’s market and reducing our average home values. However, what will the impact of the pent-up buyer’s segment be?

We’re seeing a high rate of cancellations both in the resale and new home sectors. Undoubtedly, a good percentage of these cancellations are a direct result of financial hardship due to the pandemic. We do know that a fair percentage are strategic cancellations due to a lack of consumer confidence and the willingness to wait and see if a better price will be available in the future. It’s fair to say that we will still be experiencing a housing shortage whenever we conquer this virus. It’s more than fair to say that mortgage payments will still be less than rent in many cases. It’s also incredibly fair to say that homeownership has repeatedly created more wealth for the average American than any other investment vehicle. Will the crescendo of supply and demand keep us from falling into the abyss of recession? Only time will tell. Right now it’s impossible to gauge. Anyone who claims to have a foolproof answer might just be in for a surprise at the end of the day. As the market remains on pause, it’s so early to assess or garner any movement as a trend.

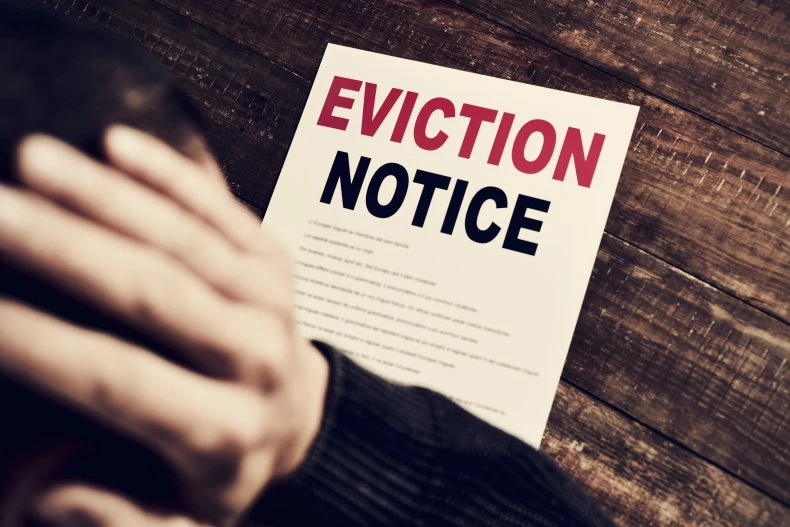

Our landlords and tenants still struggle, grappling with the balance between cash and compassion. It’s an unprecedented situation that, especially for smaller landlords, may represent an existential financial threat. But it’s also one that’s forcing rental professionals to grapple with new ways to find the balance, which is raising questions about ethics in a time of suffering. Either way, though, there’s not a single solution for landlords and renters who suddenly find themselves staring at each other across a financial chessboard. Communication is key. The CARES Act offers the same (modified version) payment deferment options in an effort to allow landlords to extend temporary relief to tenants who are suffering financial hardship. Again, this is a time-out and not a forgiveness of either a tenant’s rent or a landlord’s debt obligations. Unfortunately, we still see the news violations of the injunction running rampant.

Another man called to report that his landlord and some security guards tore out the toilet, refrigerator, television and bed in his unit to force him out when he could not make rent.

“Still, predatory landlords are harassing people at a record pace,” Bailey Bortolin, with the Nevada Coalition of Legal Service Providers told the Las Vegas Review-Journal on April 3. “Many are trying to creatively skirt the protection.”

In that same article, Heidi Foreman-Toney, a tenants’ rights counselor with Nevada Legal Services, said her phone is ringing “almost by the minute” with people “asking for advice to find out what their rights are” amid the statewide eviction moratorium. “There are just so many violations,” she told the Review-Journal. “You would think it were a movie.”

The Review-Journal reported that some [tenants] are still being served notices. Others are still being locked out. According to Foreman-Toney, one woman said her landlord started stacking plywood in the parking lot, threatening to board up units for people who can’t pay rent. Another man called to report that his landlord and some security guards tore out the toilet, refrigerator, television, and bed in his unit to force him out when he could not make rent.

While we sit at home and rifle through the endless inundation of information, rest assured that there is a $2 trillion financial response to this epidemic underway. There will likely be more – a lot more – money thrown at the recovery as all this unfolds. Unfortunately, until the virus is under control, people moving about and our businesses are reopened, all we can do is sit back and discern exactly what our next moves are. The total fallout will not be known until we reach that critical point. The consequences of this virus are shaking up the real estate industry as a whole and giving businesses the opportunity to right-size.

When you’re looking at an economy on pause as it is now you want to be able to find your new lead generation so who is the new lead generation ? EXP gives us the resources to actually go after the appropriate people based on where the economy actually is and all the other technology. We take note of where we are now and we also have the tools to know who to go after.